Graphics and CPU research consultancy Jon Peddie Research’s Q4 2021 report indicates PC GPU and CPU shipments increased modestly compared to the previous quarter but took a large hit on a year-to-year evaluation basis.

| Q4 21 vs Q3 21 | FY 21 vs FY 20 | |

| PC GPU shipments | 0.8 per cent | -15 per cent |

| PC CPU shipments | 3.9 per cent | -21 per cent |

Drilling down, JPR says single-digit quarter-on-quarter gains pale into insignificance against full-year results. Out of the 0.8 per cent gain, AMD increased shipments by 4.7 per cent, Intel by 0.6 per cent, and Nvidia took the brunt by losing 2.2 per cent.

Focussing on discrete graphics cards alone, manufactured by AMD and Nvidia add-in board (AIB) partners, shipments increased by 3.0 per cent compared to the previous quarter.

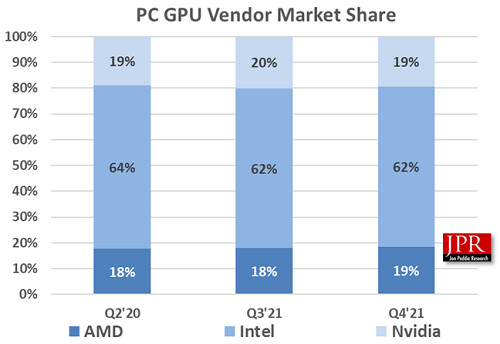

Looking at total GPU volume as a whole, Intel retains a commanding advantage over AMD and Nvidia. This may seem strange on first glance, but can easily be explained by millions of integrated GPUs shipping with Core and Celeron processors. AMD’s market share also relies heavily on integrated graphics; the situation is quite different when only taking discrete desktop and mobile graphics cards into account.

| Q2 2020 | Q3 2021 | Q4 2021 | |

| Nvidia | 82 per cent | 83 per cent | 81 per cent |

| AMD | 18 per cent | 17 per cent | 19 per cent |

If we do, Nvidia holds a 4:1 advantage that’s stayed consistent over time. Supply-side issues have stifled overall volume, as evidenced by the 15 per cent year-on-year decrease, though higher average selling prices likely offset lower shipments.

Intel is planning widespread disruption to the discrete graphics status quo this year with a line of Arc-branded cards first appearing in notebook this quarter and proliferating to desktop in Q2 2022.

In closing remarks, Jon Peddie, President of JPR, noted, “the disruptions in the supply chain caused by COVID and aggravated by Intel’s manufacturing difficulties have made forecasting unusually challenging. In this reporting period of late February, the world is facing turmoil in Ukraine, and continuing mutations of the virus, compounded by a disturbed workforce and new norms of work location. The forecast for the rest of the year is confusion and surprise.”