Laptop prices are about to rocket, according to research from tech analyst firm TrendForce. The company projects a huge increase in laptop manufacturing costs, which it predicts will end up being reflected in final store pricing. According to the analyst firm, the global laptop market is set to face dual pressures from weak demand and rising components, which could drive up prices by nearly 40%.

TrendForce notes that, since the start of 2026, laptop storage and RAM prices have risen due to tightened DRAM and NAND Flash supply. As a result, supply for some components has become increasingly uncertain, making brands’ strategic planning extremely difficult. Recent industry reports indicate that DRAM contract prices have risen by 45–50% quarter-on-quarter (QoQ) in late 2025, and analysts expect a further jump of 90–95% QoQ for the first quarter of 2026.

As if this weren’t enough, TrendForce also points out that CPU prices have begun to increase, which will be compounded by an emerging supply volatility. The latter has seemingly already begun affecting entry-level laptops across multiple brands. The firm indicates that Intel has raised some old-generation low-end CPU prices by more than 15%, which TrendForce says will be followed by mid-to-high-end chips in the second quarter of 2026.

The reason behind these price rises is, once again, AI-related chips, which are getting prioritised on advanced silicon manufacturing nodes. While AMD has apparently managed to provide a stable supply of CPUs, the report indicates a potential upcoming shortage of entry-level chips.

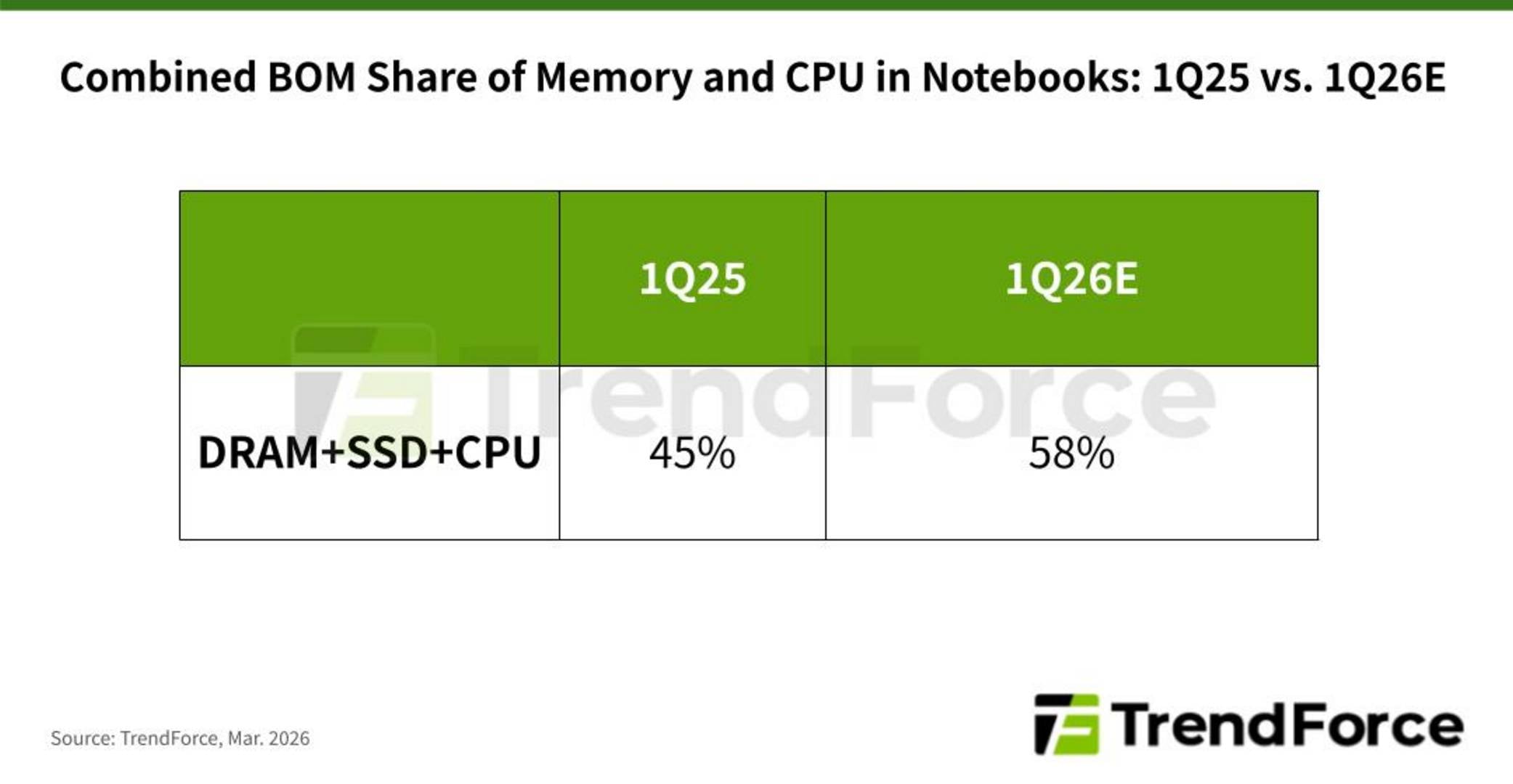

TrendForce notes that while, under normal conditions, DRAM and SSDs only account for about 15% of the total BOM (bill of materials) cost, that percentage is projected to exceed 30% in Q1 2026. As a result, a laptop costing $900 would see its retail price rise by more than 30% to account for the manufacturer’s margins. When combined with the CPU price hike, this increase could reach nearly 40% as the BOM cost of all three parts grows to represent 58% of a laptop cost in Q1 2026, compared to 45% in Q1 2025.

That said, this situation isn’t expected to impact all manufacturers to the same level. Big brands with a lot of weight in the industry may well be able to negotiate more advantageous contracts with their suppliers, thanks to larger purchase volumes. This situation could make it very difficult for small companies to maintain competitive pricing, however.